Borrower Retention Winners and Losers Last week, we shared a stat that raised a few eyebrows: Top...

Market Movers

Last week, 368 originators switched companies and 1,247 individuals obtained their NMLS license. Notable originator movements last week include:

- Jonathan Alexander ($66M, 134 units) joined SWBC Mortgage Corporation

- Kenneth Locke ($61.5M, 151 units) joined CrossCountry Mortgage, LLC

- Austin Jardine ($57.3M, 124 units) joined Barrett Financial Group, L.L.C.

- Anna Decamp ($55.6M, 90 units) joined Centennial Bank

- Breon Price ($55.3M, 175 units) joined Swift Home Loans, Inc.

- Lauren Walton ($50.2M, 110 units) joined Atlantic Coast Mortgage, LLC

- Alfonso Diaz Rojas ($48M, 123 units) joined United 1 Mortgage Corporation

- Cody Dennis ($45.2M, 57 units) joined New Day Financial, LLC

- Richard Scherer ($42.4M, 230 units) joined BoxCar Mortgage, LLC

- Louis Coppelli ($40M, 98 units) joined Forward Holdings LLC

- Senthil Kumar ($39.4M, 75 units) joined Go Rascal Inc.

Figures are based on last 14 months’ production.

Market Movers (Companies)

Top Gainers (non-Bank/CU):

- Green Lending LLC +17.02%

- Forward Holdings LLC +16.98%

- Federal First Lending LLC +13.29%

- Atlantic Coast Mortgage, LLC +8.25%

- O C Home Loans Inc. +5.44%

- Prime Choice Funding Inc. +5.42%

- Network Capital Funding Corporation +4.31%

- GRIFFIN FUNDING, INC. +4.18%

- Iconic Mortgage Corp. +3.6%

- BoxCar Mortgage, LLC +3.53%

- Gold Star Mortgage Financial Group, Corporation +3.07%

- Omni-Fund, Inc. +2.67%

- SWBC Mortgage Corporation +2.66%

Calculations based on last aggregate production of individual LO’s 14 months’ production for companies with at least 20 loan officers. Excludes companies below $100M in 14mo LO production value after gains factored in.

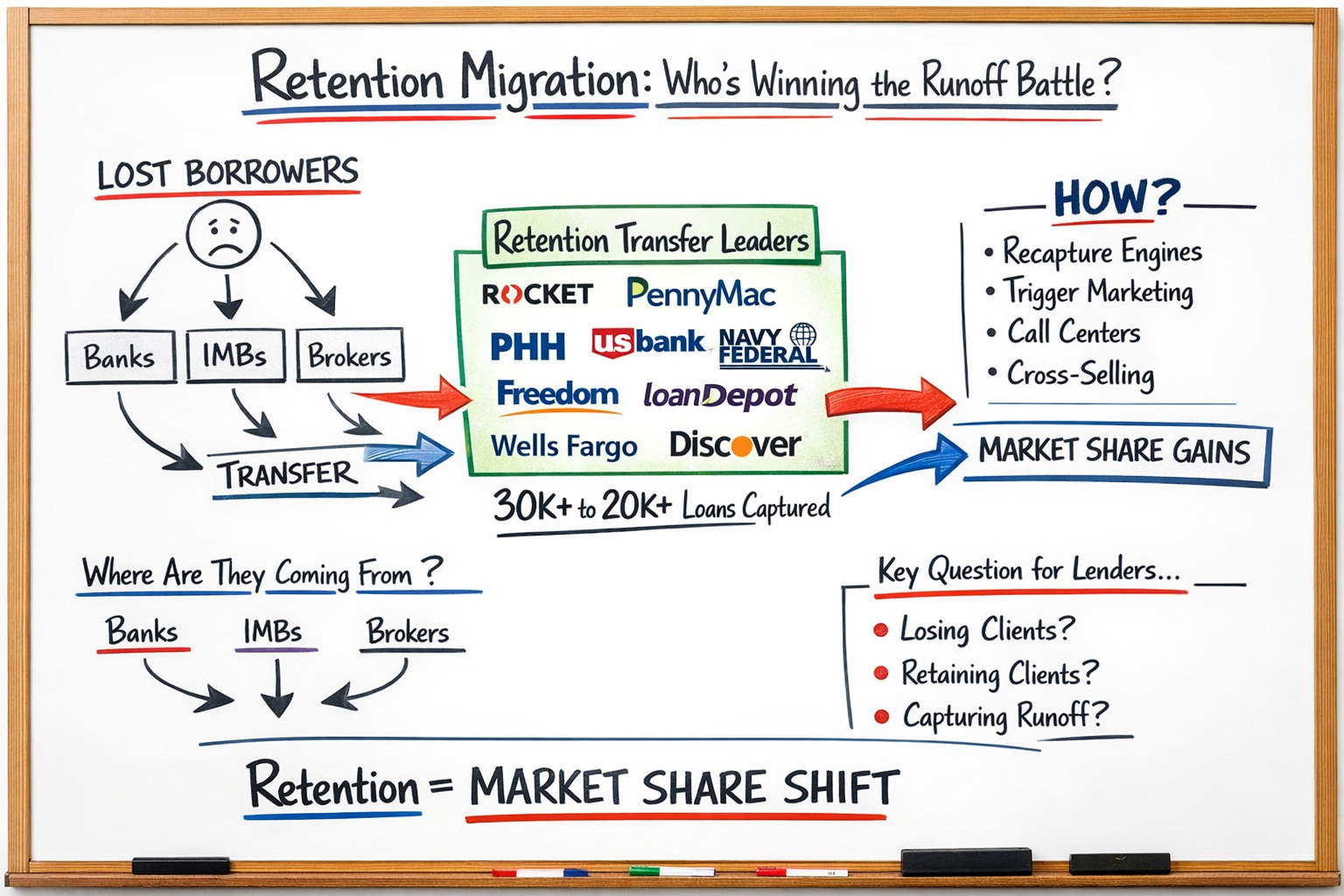

From Retention Problem to Retention Migration: Who’s Winning the Runoff Battle?

In previous articles, we focused on the borrower retention challenge.

First, we showed the scale of the industry-wide retention problem. Then we broke it down by company type and highlighted the lenders outperforming their peers.

Now we are answering the next logical question:

If so many lenders are losing repeat borrowers, who is gaining the volume?

Let’s call the winners of this battle “Retention Migration Leaders”.

Because what we are seeing is not theft. It is migration.

When one lender fails to retain a borrower, that loan does not disappear. It transfers. And the data shows that transfer of volume is highly concentrated.

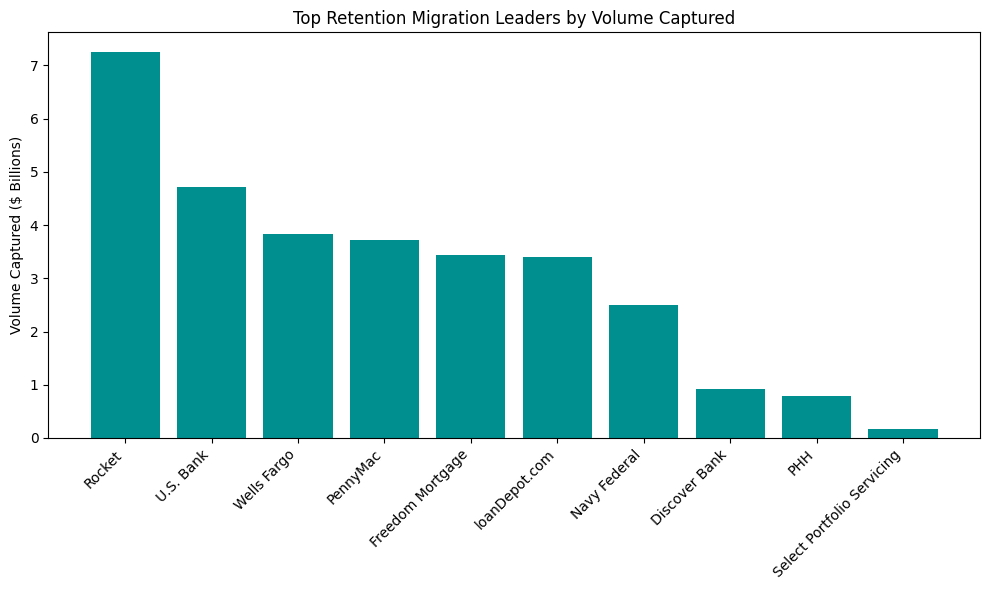

The Top Retention Migration Leaders by Volume

Across the dataset, a small group of institutions is capturing a disproportionate share of runoff dollars:

- Rocket

- U.S. Bank

- Wells Fargo

- PennyMac

- Freedom Mortgage

- loanDepot.com

- Navy Federal

- Discover Bank

- PHH

- Select Portfolio Servicing

Individually, these firms are capturing billions of dollars in loan volume that were originated by someone else.

For example:

- Rocket: approximately $7.3B in captured volume

- U.S. Bank: approximately $4.7B

- Wells Fargo: approximately $3.8B

- PennyMac: approximately $3.7B

- Freedom Mortgage: approximately $3.4B

This is not random recapture.

It is systemic market share transfer.

Where the Volume Is Coming From

When we segment the data by original company type, the pattern becomes even clearer.

From Banks:

Rocket, PennyMac, CrossCountry, and U.S. Bank are major recipients of bank runoff volume.

From IMBs:

PennyMac, PHH, Rocket, and U.S. Bank consistently capture meaningful share.

From Brokers:

PennyMac, Rocket, PHH, and servicing-driven platforms such as Nationstar and Lakeview appear prominently.

The same names repeat across categories.

That is not coincidence.

That is infrastructure and strategy.

What This Really Means

The borrower retention conversation is no longer just about defensive performance.

It is about offensive capability.

The leaders in captured volume have built:

- Sophisticated servicing-based recapture engines

- Data-driven trigger marketing programs

- Call center scale and speed

- Streamlined refinance funnels

- Aggressive cross-sell strategies

While others are still relying on manual outreach and hoping the loan officer connects in time.

The outcome is predictable.

Market share quietly consolidates toward institutions that are built to capture runoff.

The Bigger Insight

Retention is not just a loyalty metric.

It is a market share transfer mechanism measured in billions.

If your organization is not in the Migration Leader column, your volume is likely showing up in someone else’s captured total.

The Question for Lenders

Are you:

- Losing volume?

- Retaining volume?

- Or systematically capturing other lenders’ runoff?

The data shows one thing clearly.

The lenders winning in today’s market are not just surviving volume compression.

They are harvesting it.

And that is a fundamentally different strategy.

If you would like to see where your institution ranks in retention performance and whether your borrowers are staying, leaving, or transferring to specific competitors, RETR can show you.

Upcoming RETR Training

- Mon, Feb 23 @ 2p ET - Intro to RETR: The Modern Loan Officer’s Data Advantage Register

An overview of the many tools available to you in RETR – from agent and LO research, to list building and bulk contact exports, and borrower retention and refi finder tools, and more! - Wed, Feb 25 @ 12p ET - Help Your Agents Win More Offers and Listings (and Earn Their Loyalty) Register

The loan officers who grow in today’s market are the ones who bring real, tangible value. Learn how to use Track Records to help your agents win more business-and become their go-to partner because of it. - Thurs, Feb 26 @ 2p ET - Intro to RETR: The Modern Loan Officer’s Data Advantage Register

An overview of the many tools available to you in RETR – from agent and LO research, to list building and bulk contact exports, and borrower retention and refi finder tools, and more!

Is RETR Better?

When it comes to mortgage market intelligence, you have a handful of options, and RETR is one that truly stands out. Here’s what Scott Valins, Co-Founder & CEO of Go Rascal has to say about RETR: “RETR is hands-down the best data intelligence platform in the mortgage business. The UX is unmatched, the insights are actionable, and it’s become an essential growth engine for anyone in mortgage sales-loan officers, branch managers, recruiters, even CEOs. We’re proud to be true power users.”

But you don’t have to take their word for it. RETR offers a free trial to loan officers, branches, and mortgage companies to judge the quality of the data and insights for themselves.